Originally published at: Iran conflict exposes America's Achilles' heel - FreightWaves

Diesel prices have spiked to $5.96 per gallon in premium markets as escalating Middle East tensions collide with America’s crumbling refinery base. The surge comes at a critical inflection point for trucking, with tender rejection rates climbing and capacity tightening after a brutal four-year freight recession, raising questions about whether the industry can capitalize on the recovery when fuel costs threaten to erase margin gains.

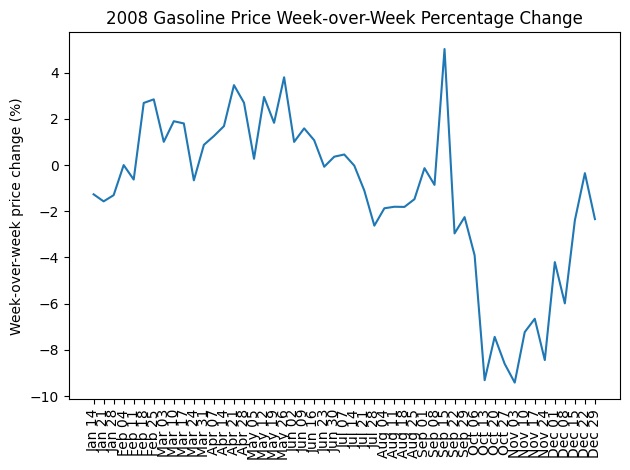

A little History lesson about fuel shocks. This is a graph showing week-over-week percentage changes in the price of fuel. Fuel shock was a main driver of the 2008 Recession.

The key lesson from 2008 is that the greatest economic danger from fuel is not simply high prices—it is extreme volatility. Businesses can usually adapt to expensive fuel if the price is stable. They can adjust contracts, fuel surcharges, inventory planning, and transportation budgets. What they cannot adapt to is fuel that moves so quickly that costs change faster than shipments can be priced.

In 2008, fuel prices rose sharply over a short period, with repeated weekly increases large enough to outrun normal freight pricing mechanisms. Trucking contracts and fuel surcharges lag actual pump prices, often by one or two weeks. When prices jump faster than those mechanisms can adjust, transportation companies suddenly face major cost exposure. For many carriers operating on thin margins, even a modest weekly fuel jump can erase profitability on a shipment already in transit.

Once this happens, the effects spread through the supply chain. Shippers begin delaying orders because they cannot predict the final landed cost of goods. Distributors hesitate to move inventory. Manufacturers shorten purchasing cycles or reduce shipments. Freight volumes begin slowing—not necessarily because demand has disappeared, but because businesses lose confidence in their cost assumptions.

This is exactly what many operators in trucking and logistics observed during the summer of 2008. A shipment loaded on Monday for delivery two days later could arrive with fuel costs meaningfully different than when the freight was priced. When landed costs become uncertain, rational businesses slow down shipments until pricing stabilizes.

The result is a cascading effect. First, transportation margins compress. Then freight volumes weaken. Inventory planning becomes more defensive. Credit risk increases across transportation and logistics providers. Eventually the instability spreads into broader economic activity.

Where we are today is very different—at least for now. Recent fuel data shows prices fluctuating within a relatively narrow range and week-over-week changes generally remaining modest. That means businesses can still plan shipments, price contracts, and manage fuel surcharges with reasonable confidence. In other words, the fuel market is moving, but it is not yet destabilizing the logistics system.

The broader economic lesson is clear. Fuel price levels matter, but fuel volatility matters far more. Transportation is the circulatory system of the economy. When fuel becomes so unstable that businesses cannot reliably estimate the cost of moving goods, commerce slows, freight hesitates, and the wider economy eventually follows. The key risk going forward is not simply higher fuel prices—but whether volatility returns at a scale that again disrupts the pricing logic of commerce.